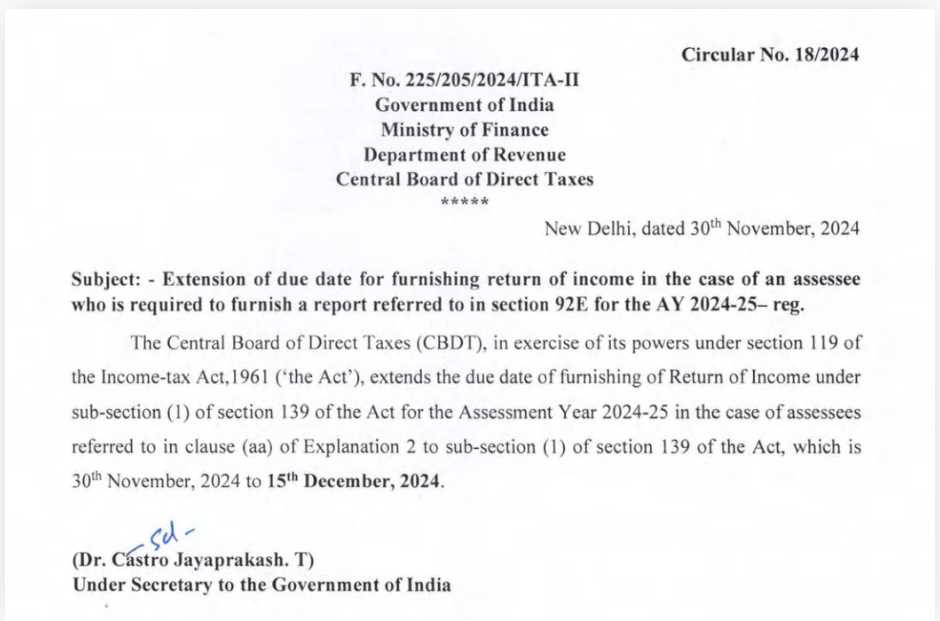

The Government of India has further extended the due date for filing Form 3CEB under Section 92E of the Income Tax Act up to 15th December 2024. This decision provides considerable relief to taxpayers, especially those involved in international transactions or specified domestic transactions.

In this blog, we will explain what Section 92E entails, the importance of Form 3CEB, and how the new deadline impacts businesses.

Know Your Section 92E of the Income Tax Act (H2)

Section 92E requires entities undertaking international transactions or specified domestic transactions to furnish a Transfer Pricing Report in Form 3CEB. According to this section, the report must be certified by an eligible Chartered Accountant (CA).

Important Notes on Form 3CEB

- Purpose: To prepare and submit information about transactions involving associated enterprises, aimed at preventing the shifting of profits.

- Required Information: Details on the nature, value, and methodology adopted in arriving at the arm’s-length price of transactions.

- Certification: Certified by a Chartered Accountant to ensure proper and accurate compliance.

Extended Date for FY 2023–24

Previously, Form 3CEB was required to be submitted by 31st October 2024. The extension to 15th December 2024 offers six additional weeks for businesses to prepare their documentation.

Advantages of the Extension

- Providing Extra Time for Accurate Representation: Financial facts must be critically analyzed and reviewed.

- Avoiding Last-Minute Errors: Submitting before the revised deadline helps avert penalties.

- Ensuring Compliance with Transfer Pricing Laws: The extension supports compliance while minimizing errors.

Extended Date for FY 2023–24

Previously, Form 3CEB was required to be submitted by 31st October 2024. The extension to 15th December 2024 offers six additional weeks for businesses to prepare their documentation.

Advantages of the Extension

- Providing Extra Time for Accurate Representation: Financial facts must be critically analyzed and reviewed.

- Avoiding Last-Minute Errors: Submitting before the revised deadline helps avert penalties.

- Ensuring Compliance with Transfer Pricing Laws: The extension supports compliance while minimizing errors.

Who Needs to File Form 3CEB?

Applicable Entities

- Companies with International Transactions: Entities that engage in the cross-border transfer of goods, services, or intangibles.

- High-Value Domestic Transactions: Indian domestic transactions exceeding specified thresholds.

Penal Provisions for Non-Filing

Failure to file Form 3CEB or missing the due date can lead to the following consequences:

- Penalty: ₹1,00,000 for failure to furnish the report.

- Increased Scrutiny: Additional taxes or penalties may be imposed during assessments.

How to Prepare for the Revised Date

- Gather Transaction Data: Compile details of related-party international and domestic transactions.

- Consult a Chartered Accountant: Seek professional assistance for proper documentation and certification.

- Use Technology for Accuracy: Leverage tools to analyze and validate transfer pricing methodologies.

- Stay Updated: Monitor notifications and circulars issued by the Income Tax Department.

Key Takeaways for Businesses

The extension of the due date to 15th December 2024 for filing Form 3CEB is a welcome move for businesses dealing with complex transfer pricing regulations. Companies should use this additional time wisely to ensure compliance and avoid penalties.

At Power of Factorial Business Solutions, we provide expert guidance on Income Tax and transfer pricing compliance. Connect with us at +91 81050 21287 for individualized support.